Introduction

If you run a small business and you have ever felt like your workers comp bill came out of nowhere, you are not alone. Many business owners get caught off guard by large upfront payments or surprise bills at audit time. That is exactly why so many people are now turning to pay as you go workers comp as a smarter, more flexible option.

Pay as you go workers comp lets you pay your insurance premiums based on your actual payroll each pay period instead of making one big payment at the start of the year. It is a simple idea that can make a huge difference for your cash flow and your peace of mind.

In this guide, we will walk through everything you need to know about pay as you go workers comp, including how it works, who it is for, what it costs, and whether it is the right fit for your business.

What Is Pay As You Go Workers Comp? (Quick Answer)

Pay as you go workers comp is a payment method for workers compensation insurance. Instead of paying a large estimated premium at the start of the policy year, you pay smaller amounts each time you run payroll.

Your payroll provider or insurance carrier calculates what you owe based on your actual wages for that pay period. This means your payments go up when you hire more workers and go down when business slows. It matches your real situation instead of a guess made months in advance.

How Pay As You Go Workers Comp Works

The process is pretty straightforward. Here is a step by step look at how it works:

Step 1: You sign up for a workers comp policy that uses the pay as you go method.

Step 2: Every time you run payroll, the system pulls your payroll data.

Step 3: Your premium is calculated based on the wages paid, the type of work your employees do, and your state rates.

Step 4: The payment is automatically collected, either through your payroll provider or directly by your insurer.

Step 5: At the end of the year, an audit is done to confirm the final numbers, and you either get a small refund or owe a small amount.

This cycle keeps everything accurate and up to date throughout the year.

Traditional Workers Comp vs Pay As You Go Plans

Most business owners have dealt with traditional workers comp at some point. Here is how the two approaches compare:

| Feature | Traditional Workers Comp | Pay As You Go Workers Comp |

|---|---|---|

| Upfront payment | Large estimated premium due at start | Little to no upfront payment |

| Premium accuracy | Based on payroll estimates | Based on actual payroll each period |

| Cash flow impact | High upfront cost strains cash flow | Payments spread evenly throughout year |

| Year-end audit | Often results in large bills or refunds | Smaller audit adjustments |

| Flexibility | Fixed regardless of payroll changes | Adjusts automatically with payroll |

| Best for | Stable, predictable payrolls | Seasonal or growing businesses |

As you can see, pay as you go workers comp takes the guesswork out of premium payments.

Why Small Businesses Choose Pay As You Go Workers Comp

Small businesses love this option for several reasons.

First, cash flow is everything when you are running a small operation. Having to write a big check at the start of the year for a traditional policy can be painful, especially if business is slow. Pay as you go workers comp lets you spread those costs out.

Second, many small businesses have seasonal workforces. A landscaping company might have 20 workers in the summer and 3 in the winter. With the traditional method, you might overpay for months when workers are not even on the payroll. Pay as you go workers comp fixes that problem.

Third, it is simply easier to manage. When your insurance payments are tied to your payroll runs, you do not have to think about them separately. It becomes part of your regular payroll routine.

How Payroll Affects Workers Comp Costs

Your workers comp premium is almost always tied to your payroll. The more wages you pay out, the higher your premium. This is true for both traditional and pay as you go workers comp, but the key difference is timing.

With a traditional plan, your insurer estimates what your total payroll will be for the year and charges you upfront based on that guess. With pay as you go workers comp, you report your actual payroll as you go, so the premium reflects what is really happening in your business.

Other factors that affect costs include:

The type of work your employees do. Roofers and electricians carry higher risk than office workers, so their rates are higher.

Your claims history. Businesses with fewer past claims usually pay lower rates.

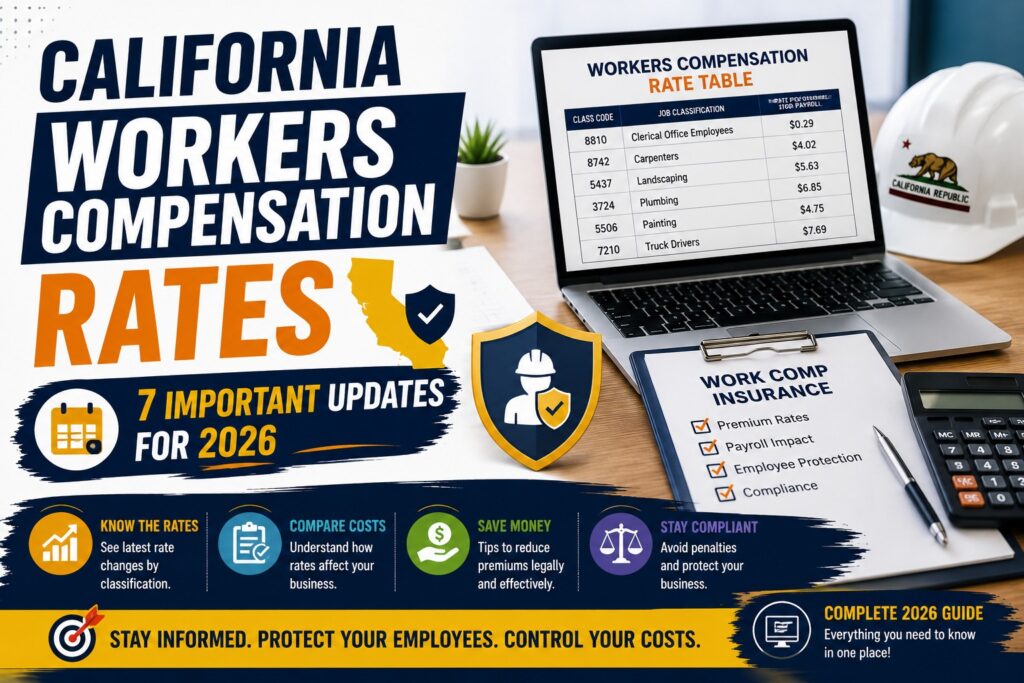

Your state. Workers comp rates vary a lot depending on where your business operates. You can learn more about how rates work by reading about California workers compensation rates and how state rules play a role.

Benefits of Pay As You Go Workers Comp

There are quite a few solid reasons to consider this type of plan.

Better cash flow management. Since you are paying smaller amounts more often instead of one large chunk, your bank account stays healthier throughout the year.

More accurate premiums. Because your payments are based on real payroll data, you are rarely overpaying or underpaying.

Fewer audit surprises. Traditional plans often lead to big bills or refunds at audit time because the estimate was too high or too low. Pay as you go workers comp reduces that problem significantly.

Easier bookkeeping. When your insurance costs line up with your payroll cycles, your records are cleaner and easier to manage.

Flexibility during growth. If you hire more workers mid-year, your premium adjusts right away rather than waiting for a renewal or mid-term adjustment.

Possible Downsides Business Owners Should Know

Pay as you go workers comp is not perfect for everyone. Here are a few things to think about.

Some carriers charge slightly higher rates for the convenience of the pay as you go structure. You might pay a small premium for the flexibility.

If you have a very stable and predictable payroll, the traditional method might actually work just fine for you. In that case, the pay as you go model may not offer much of an advantage.

Integration with your payroll system is required. If you run payroll manually or use older software, setting up pay as you go workers comp might take some extra work.

Also, not all insurance carriers offer this option, so you may have fewer choices depending on your state and industry.

How Monthly Premium Payments Are Calculated

Your pay as you go workers comp premium is calculated using a simple formula:

Payroll for the period divided by 100, then multiplied by the rate for your job classification code.

For example, if you pay out 10,000 dollars in wages and your rate is 2.00 per 100 dollars of payroll, your premium for that period would be 200 dollars.

Each type of job has its own classification code and rate. Office workers have much lower rates than construction or warehouse workers. Rates also differ by state.

To get a sense of what you might pay, you can use the Workers Compensation Insurance Calculator to run some numbers based on your payroll and job types.

Industries That Commonly Use Pay As You Go Workers Comp

Pay as you go workers comp is popular across many industries, but especially in ones where headcount changes throughout the year.

Construction. Project based work means crews grow and shrink regularly.

Restaurants and hospitality. Staff changes with the season and with events.

Landscaping and agriculture. Strong seasonal swings make fixed premiums frustrating.

Retail. Holiday seasons bring in temporary workers who are gone by January.

Staffing agencies. The whole business model involves constantly changing employee counts.

Healthcare staffing. Contract workers and rotating shifts make payroll unpredictable.

If your business falls into any of these categories, pay as you go workers comp is worth a serious look.

Does Pay As You Go Reduce Audit Problems?

Yes, and this is one of the biggest reasons businesses make the switch.

With a traditional workers comp plan, your insurer estimates your annual payroll at the start of the year. At the end of the year, an audit compares the estimate to what you actually paid out. If you paid more in wages than expected, you owe more. If you paid less, you get a refund.

These audit adjustments can be large and unexpected. Some businesses end up owing thousands of dollars at audit time, which puts a real strain on their finances.

Pay as you go workers comp largely solves this because you are already reporting real payroll data every pay period. The numbers are always current, so the audit adjustment at the end of the year is usually very small.

Can It Help Businesses Manage Cash Flow Better?

Absolutely. This is probably the number one reason small business owners switch to pay as you go workers comp.

Think about a construction company that does most of its work in spring and summer. With a traditional plan, they might owe a large premium in January when cash is tight. With pay as you go workers comp, their premiums are low in winter when they have fewer workers and higher in summer when the crew is full.

That kind of flexibility makes a real difference. It means you are not draining your bank account during slow months just to keep your coverage active. You can read more about how workers comp costs and benefits work by checking out how to work out workers compensation, which walks through the calculation process in simple steps.

Common Mistakes Employers Make With Workers Comp Payroll

Even with pay as you go workers comp, there are some common mistakes that can cost you.

Misclassifying employees. Putting workers in the wrong job classification code leads to incorrect premiums and audit problems. Make sure your employees are classified correctly based on the work they actually do.

Forgetting to include all types of compensation. Tips, bonuses, overtime, and some allowances may count as payroll for workers comp purposes depending on your state.

Not updating your payroll system when you hire or let go of workers. Since pay as you go workers comp is tied to payroll data, any errors in your payroll records will flow through to your premiums.

Assuming all states work the same way. Workers comp rules and rates vary by state, so what works in one state may not apply in another. Understanding your state is key.

How to Choose the Right Workers Comp Insurance Plan

Choosing the right plan comes down to your specific situation. Here are a few questions to ask yourself:

Does your payroll change a lot throughout the year? If yes, pay as you go workers comp is probably a better fit than a traditional plan.

Do you have cash flow challenges during certain months? If big upfront payments are hard to handle, pay as you go makes life easier.

Does your payroll system support automatic data sharing with insurers? Most modern payroll platforms do, which makes setup simple.

Are you willing to compare carriers? Not all insurers offer pay as you go workers comp, so shop around to find the best rate and terms.

Real Examples of Pay As You Go Workers Comp Costs

Here are some simple examples to make the numbers real.

Example 1: A small restaurant with 8 employees pays out about 15,000 dollars in wages every two weeks. Their workers comp rate is 1.50 per 100 dollars. So each pay period, their premium is about 225 dollars. That is very manageable compared to a lump sum at the start of the year.

Example 2: A landscaping company with a crew that grows from 4 workers in winter to 18 in summer. In winter they might pay 80 dollars per pay period. In peak summer, that climbs to around 500 dollars. With pay as you go workers comp, those swings match their cash flow naturally.

Example 3: A construction firm with a 50,000 dollar payroll per month and a rate of 5.00 per 100 dollars pays 2,500 dollars per month. Spread across 12 months, that is much easier to handle than a 30,000 dollar payment in January.

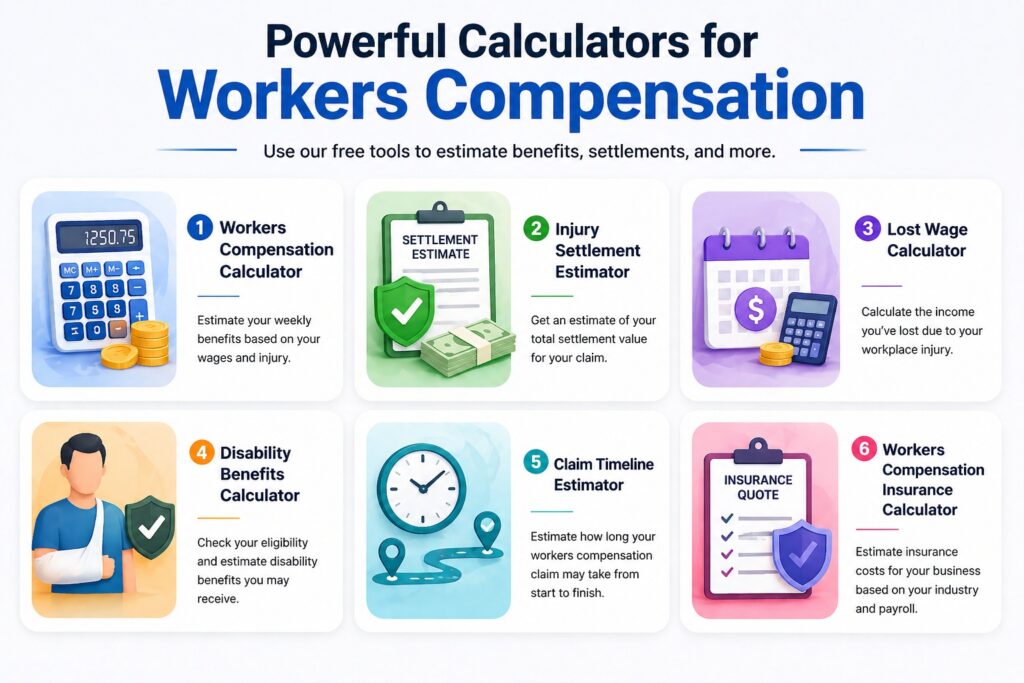

Workers Comp Insurance Calculator Tools

Trying to figure out what pay as you go workers comp might cost your business? These tools can help:

Workers Compensation Insurance Calculator helps you estimate your annual premium based on payroll and job type.

Workers Compensation Calculator helps employees understand what benefits they might receive if they are injured on the job.

These tools are free and easy to use. They give you a starting point so you can plan ahead and avoid surprises.

Secure Your Retirement Start Planning from now! Retirement Saving Calculator

FAQs (Common Questions)

Is pay as you go workers comp more expensive than traditional plans?

Not always. In many cases the total cost is similar or even lower because you avoid overpaying on estimates. The main benefit is how the payments are timed, not necessarily how much you pay overall.

Does every state allow pay as you go workers comp?

Most states do, but rules and available carriers can vary. Check with a local insurance broker to confirm what is available in your state.

Can I switch from a traditional plan to pay as you go mid-year?

In many cases yes, though the transition may require your current policy to be cancelled and a new one started. Talk to your insurer about the specifics.

Do I still need an audit with pay as you go workers comp?

Yes, most policies still require a year-end audit, but because your payments are already based on real payroll data, the adjustments are usually very small.

What payroll systems work with pay as you go workers comp?

Most major payroll platforms like Gusto, ADP, Paychex, and QuickBooks integrate with pay as you go workers comp providers. Ask your carrier which systems they support.

What happens if I underreport payroll?

Underreporting payroll, even accidentally, can lead to penalties and a large audit bill. Always make sure your payroll records are accurate before each submission.

Conclusion

Pay as you go workers comp is one of the smartest tools available for small and medium sized businesses that want more control over their insurance costs. Instead of making one large estimated payment and hoping the numbers work out, you pay based on what is actually happening in your business each pay period.

It reduces the risk of audit surprises, helps with cash flow, and keeps your premiums aligned with your real payroll. Whether you run a restaurant, a landscaping company, a construction firm, or any business where your team size changes throughout the year, pay as you go workers comp gives you the flexibility you need.

If you are ready to explore your options, start by getting a few quotes from carriers that offer pay as you go workers comp in your state. Use the Workers Compensation Insurance Calculator to estimate your costs and go into those conversations informed.

Have questions about your workers comp coverage or want to share your experience with pay as you go workers comp? Drop a comment below or reach out for help. Making the right choice now can save you money and stress all year long.