When a workplace injury happens, figuring out how to work out workers compensation benefits can feel overwhelming. This guide breaks down step-by-step how indemnity pay is calculated, with examples and expert tips. We’ll show you how to compute your Average Weekly Wage (AWW), apply the proper formula, and understand state limits so you’re not left guessing. Whether you’re an injured employee or an employer, these clear explanations and tables will make the process understandable. By the end, you’ll know exactly how to work out workers compensation in your situation and avoid common pitfalls.

workers-comp

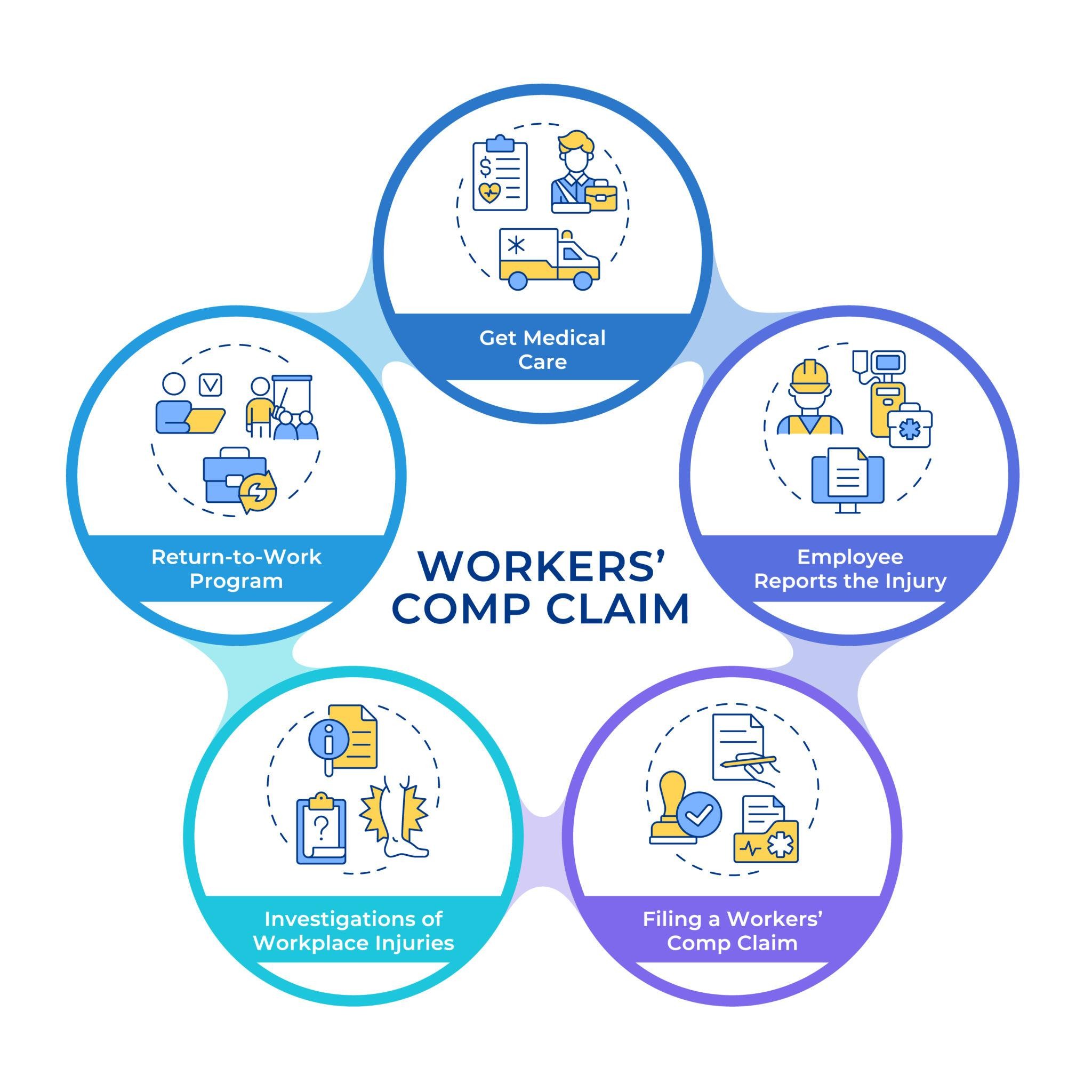

What Does “Work Out Workers Compensation” Mean?

To “work out” workers’ compensation simply means determining your benefit amount after a job injury. In practice, it’s about calculating your weekly wage-loss benefits under state law. For example, a Georgia lawyer explains that your workers’ comp benefit is “the average of your weekly salary over the 13-week period” before injury. In other words, you gather your past pay, average it as required, and apply the state’s rate (often two-thirds). So asking “how to work out workers compensation” is really asking: How do I calculate the weekly check I’ll receive?

Almost every calculation starts with the Average Weekly Wage (AWW) – your typical earnings before the accident. As New York’s Workers’ Compensation Board explains, “Your average weekly wage is based on your earnings for the 52 weeks prior to the date of injury”. Texas, by contrast, looks at 13 weeks: “Your AWW is the average amount of money your employer paid you each week in the 13 weeks before your injury or illness”. Once you know your AWW, you multiply it by the state’s benefit rate (usually around 66.67%) to get your weekly compensation. In short, “working out” workers’ comp means following these legal steps to get to your final benefit number.

How Workers Compensation Is Calculated

Understanding how to work out workers compensation is essential if you want to estimate your benefits accurately. Calculating workers’ compensation typically involves two main steps: (1) computing the Average Weekly Wage (AWW), and (2) applying the compensation formula (a percentage of that AWW). While each state has its own rules, the overall process is quite similar.

Determine your AWW:

Start by collecting your gross earnings for the period required by law. Many states use the last 52 weeks (1 year) of pay, while others, like Texas, may use 13 weeks. For seasonal or new workers, special rules may apply, such as using a similar employee’s earnings. Always use gross wages (before taxes or deductions), since AWW is based on total income earned.

Apply the percentage:

Once your AWW is calculated, multiply it by the state’s benefit rate. Most states pay about two-thirds (≈66.67%) of your AWW for total disability. For example, Georgia uses a fixed two-thirds rate, while Massachusetts may pay around 60% for certain cases. Texas uses slightly different percentages depending on the benefit type. When learning how to work out workers compensation, this step is key, as it determines your estimated weekly payment, subject to state maximum and minimum limits.

Workers’ Compensation Formula (Basic Calculation): Once AWW is established, the basic indemnity formula is usually:

javaCopyWeekly Benefit = (AWW) × (Benefit Rate)

For example, if your AWW is $900 and the rate is 66.67%, you’d get about $600/week. As one Georgia attorney notes, “the compensation rate is two-thirds of the calculated average weekly wage”. In Pennsylvania, benefits are also “two-thirds of their weekly wage” subject to state caps. Massachusetts pays 60% of AWW for Temporary Total Disability and 66⅔% for Permanent Total Disability. Note that some workers get different rates for partial disability or death – Texas, for instance, uses 80% of AWW for Supplemental Income Benefits and 75% for lifetime/death benefits. Always check your state’s schedule (see table below).

Example Calculation (Real Case): Let’s illustrate with New York’s rules. Suppose Jane worked 5 days a week, earned $45,000 last year, and was paid for 250 days. New York law says AWW = (gross salary ÷ days worked) × 260 ÷ 52. Using Jane’s figures: ($45,000 ÷ 250 days) = $180 average daily wage; $180 × 260 = $46,800 annualized; then $46,800 ÷ 52 = $900 AWW. Her weekly benefit (two-thirds of AWW) would be $600. (In fact, NY’s Board example confirms this: “AWW would be set at $900” for $45k over 250 days.)

For a Georgia example: John earned $13,000 in the 13 weeks before injury (exactly 13 full weeks of work). His AWW = $13,000 ÷ 13 = $1,000. Georgia pays 2/3, so John’s weekly comp would be about $667. Georgia also caps benefits; after July 2019 the maximum is $675/week, so John would receive $667 (below the cap). If he were in Massachusetts earning the same AWW of $1,000, his Temporary Total rate would be 60% ($600) and Permanent Total 66.7% ($667), subject to the MA max of ~$1,829.

State Differences in Calculation

Workers’ comp laws vary widely by state. The table below compares a few examples of how AWW and benefits differ. Note that AWW basis can be 52 weeks (1 year) or 13 weeks (Texas, many Southern states), and benefit rates can range from 60% up to 100% for certain benefits. The max weekly benefit is set by law and usually adjusts annually (as shown for 2025/26).

| State | AWW Calculation | Benefit Rate | Max Weekly Benefit (approx.) |

|---|---|---|---|

| New York | Based on last 52 weeks of gross wages (using a “days-worked” formula: 5-day workers use 260× method) | 66.7% of AWW | $1,222 (for 7/2025–6/2026) |

| Pennsylvania | 52 weeks of gross earnings (or wage data) | 66.7% of weekly wage | $1,394 (effective Jan 2026) |

| Georgia | 13 weeks of wages (one-thirteenth of gross 13-week total) | 66.7% of AWW | $675 (flat cap for post-2019 accidents) |

| Texas | 13 weeks of wages | TIB: 70% of AWW; LIB: 75%; SIB: 80% | $1,271 (TIB max for FY2026) |

| Massachusetts | 52 weeks of wages | TTD: 60% of AWW; Perm Total: 66.7% | $1,829.13 (100% of SAWW in 2025) |

Each state’s rules have nuances (e.g. New York uses 300× for 6-day workweek, 200× for seasonal , Illinois adds 133.33% of state AWW for max, etc.). But the common pattern is: calculate your AWW by averaging your past earnings, then multiply by a set percentage, and apply any minimum/maximum limits. Consult your state’s workers’ comp board or labor office for specific formulas.

Factors That Affect Your Compensation Amount

Many factors beyond just your pay rate will affect the final benefit. Keep these in mind when figuring your comp:

- Wage history details: Overtime, bonuses, commissions and fringe benefits often count. Texas explicitly includes overtime and things like health insurance or car allowances in AWW. Conversely, failing to include consistent overtime or bonus pay can understate your AWW. One Illinois guide warns that “Leaving out some forms of your income during the calculation process lowers your average weekly wage”.

- Weeks/days worked: If you missed work (e.g. vacations or unpaid leave), some states deduct those weeks. Illinois deducts weeks off if you missed more than 5 days. New York adjusts by how many days you actually worked: a 5-day schedule uses a 260 multiplier, 6-day uses 300, and seasonal workers use 200. Using the wrong method here can mis-calc your AWW.

- Length of employment: If you worked less than the state’s base period (e.g. under 52 weeks), most states use a shorter timeframe or a “similar employee” workaround. For instance, Georgia says if you haven’t worked 13 weeks, they’ll use a coworker’s data. Not accounting for this can lead to errors.

- Concurrent jobs: If you had more than one job when injured, some states let you include both incomes. For example, New York allows adding wages from another employer if your injury stops you from working there. Texas lets you report a second job as well.

- Career advances: States sometimes account for age or expected raises. New York provides a “wage expectancy” bump for workers under 25, effectively raising the AWW. Make sure pay raises or promotions just before injury are included; omitting a recent raise is a common mistake that “will lower and [be] inaccurate”.

- Type of disability: Whether you’re totally or partially disabled affects payments. In partial disability, some states pay a percentage of the wage difference. Always apply the correct subtype (total vs partial).

- Statutory caps and floors: Each state sets its own minimum and maximum weekly rates. For example, Massachusetts now guarantees at least 20% of the State AWW, and Pennsylvania pays 90% of wages for very low earners. These limits can raise or lower your actual pay relative to the basic formula.

In short, don’t overlook any income or eligibility rules. A skilled workers’ comp attorney or adjuster will comb through your pay stubs, job records, and the law to make sure nothing is missed. Understanding these factors helps you work out your workers compensation more accurately from the start.

Maximum and Minimum Benefit Limits

After calculating your raw benefit, remember that state law caps it. Every state sets minimum and maximum weekly comp rates which automatically apply:

- Max benefit: This is the highest weekly payment allowed. For instance, New York’s max benefit in 2025/26 is about $1,222/week. Pennsylvania’s max was $1,394 in 2026. Georgia’s is a flat $675 (for all post-2019 injuries). Texas’s max for TIB (70% of AWW) is $1,271 (FY2026). These maximums are usually tied to the State Average Weekly Wage (SAWW) and change yearly. If your calculated benefit exceeds the max, you only get the max.

- Min benefit: There’s usually a floor too. Massachusetts law, for example, sets a minimum comp rate at 20% of SAWW (roughly $366/week in 2025). Pennsylvania’s schedule pays 90% of AWW for very low earners, effectively ensuring even the lowest wages get a high replacement rate. Some states guarantee a small flat minimum (like Illinois’s minimum based on household status).

Keep these in mind when working out your workers compensation: your actual check may be capped or floored by law. If your AWW is very high, expect the benefit to top out at the state maximum. If your AWW is very low, your pay might actually be higher than two-thirds thanks to a guaranteed floor or percentage.

🔧 Workers Compensation Calculator (Estimate Your Pay)

While the official method is to follow the state rules above, you can use a simple “calculator” approach to get a quick estimate:

- Gather pay data: Total your gross earnings for the calculation period (52 weeks for most states, 13 weeks for states like Texas). Include overtime, bonuses, etc. If you had two jobs, add both salaries if allowed.

- Compute AWW: Divide that total by 52 (or 13) to find your average weekly wage. Example: If your 52-week total was $52,000, then AWW = $1,000.

- Apply the rate: Multiply AWW by your state’s comp percentage. In many states it’s 2/3 (66.7%). If your AWW was $1,000, that gives $667/week.

- Check state caps: If that result is above your state’s max or below its minimum, adjust to the cap/floor. For instance, if Texas’s max is $1,271 and you got $1,300 by formula, you’d only receive $1,271.

- Adjust for specifics: If you have partial disability, use the partial formula (often 2/3 of the difference in wages). If you’re filing a lump-sum settlement, multiply the weekly figure by 52 (one year) to approximate an annual amount.

For example calculation: If your AWW is $800 and your state pays 66.7%, your gross weekly benefit estimate is $533. If your state’s max is $600, you get the full $533. If it were above $600, you’d be capped at $600.

This rough “calculator” gets you in the ballpark. Many state agencies and law firms offer interactive calculators too. But always double-check with actual pay records and consider consulting an expert, because every detail (like overtime or separate jobs) can shift your result.

Common Mistakes When Calculating Workers Comp

Even small errors can change your compensation significantly. Here are mistakes to avoid when you work out workers’ compensation:

- Using Net Instead of Gross Wages: Workers’ comp uses gross wages. Do not base calculations on your take-home pay. Texas law explicitly says AWW is calculated using gross wages. If you accidentally use net (after-tax) amounts, you’ll under-calc your benefits.

- Excluding Income Sources: Don’t forget overtime, commissions, bonuses, or employer-paid perks. Illinois attorneys warn that “leaving out some forms of your income… lowers your AWW”. For example, if you regularly earned overtime pay, include it. If you got a year-end bonus, include it in that year’s wages when averaging.

- Miscounting the Time Period: Forgetting to adjust for lost weeks (vacation, sick leave) can distort the average. Illinois law allows deducting unpaid leave beyond a few days. If you had a long break, count only actual worked weeks in your total before dividing. Similarly, if you worked less than a full year, make sure you apply the “less than full period” method (e.g. divide by 13 weeks or use a coworker’s record).

- Ignoring State Multipliers: In New York, using the wrong multiplier for your schedule is common. A five-day worker uses a 260-day multiplier, but a six-day worker uses 300, and a seasonal worker uses 200. Applying the wrong one will miscalculate your AWW.

- Not Applying Wage-Expectancy or Dual-Job Rules: If you qualify for special rules (NY’s under-25 wage expectancy, combining concurrent wages, etc.), make sure to use them. Failing to apply a legal “boost” or ignoring secondary employment income is a loss. (For example, NYC’s WCB allows adding a second job’s pay into AWW.)

- Taking the Insurer’s Word: Insurers may give you a quick estimate. Always double-check their math. Mistakes happen, and one tip is to calculate your own estimate using the steps above. If you find a discrepancy, you have evidence to support raising your AWW.

- Calculate Your Worker Compensation with our Accurate Tool or Explore Useful Tools

- Retirement calculator

By avoiding these errors, you ensure your workers compensation workout is accurate. When in doubt, consult the guidelines or get help – a small mistake in your AWW can cost thousands over time.

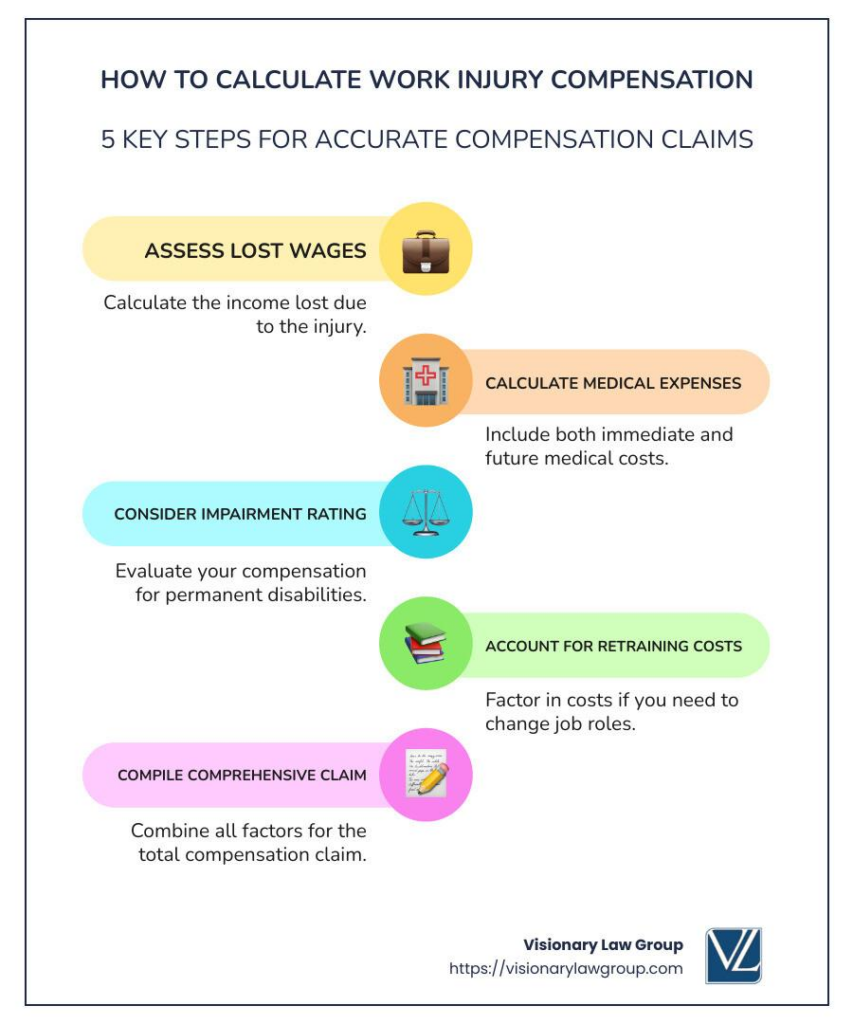

How to Estimate Your Settlement Amount

If you settle or take a lump sum, you’ll also want to estimate that value. While formulas vary, one rule-of-thumb is: annualize your wage loss and add for future costs. In plain terms, multiply your weekly benefit by 52 to get the yearly wage-replacement value. Then consider any extra years of disability or medical care. This is an important part of understanding how to work out workers compensation accurately.

For example, Rad Law Firm suggests a basic approach: “Typically, … taking your weekly wage loss and multiplying it by 52… is a general estimate of what the insurance company will pay for wage loss benefits”. So if your weekly benefit is $500, that’s $26,000 per year of loss. If you have lifelong injury, an attorney might multiply by expected years of disability or use present-value tables. You’d then add the present value of expected medical treatments or future needs (like home care).

In practice, lawyers use tables and life expectancy factors to refine this estimate. But the key takeaway is to start with your weekly benefit × 52 and then work with a professional for the complex part. This ensures you don’t undervalue your claim.

FAQs (Common Questions)

- Q: What exactly is “Average Weekly Wage”?

A: AWW is simply your typical pre-injury pay, averaged over the period set by law. It includes your base salary plus any regular overtime or bonuses. For instance, Texas defines AWW as your 13-week pay divided by 13, while New York uses 52 weeks. - Q: How much of my wage will Workers’ Comp pay?

A: Most states pay around 66.67% (two-thirds) of AWW for full disability. A few (like MA for TTD) use 60%, and Texas pays 70% or higher for some benefit types. There’s almost always a legal cap (max) on the weekly payment, so even high earners are limited to that maximum. - Q: Are Workers’ Compensation benefits taxable?

A: Generally, no. State laws typically treat the benefit as tax-free (unlike regular wages). For example, New York law explicitly notes these benefits are “tax exempt” and paid at a “33% reduction from the employee’s gross salary” (i.e. 66.7% of gross). This tax advantage is one reason workers’ comp pays only a portion of your pay instead of 100%. - Q: What if I had only part-time or seasonal work?

A: Most states prorate your wages to reflect your schedule. For example, if you worked fewer than 52 weeks, your actual weeks worked are used in the average. If you worked less than the base period (13 or 52 weeks), many states substitute a similar worker’s pay. Always report exactly what you earned; the formula will adjust. - Q: Can I include second jobs or tips?

A: Often yes, if the work was concurrent. New York allows adding a second concurrent job’s wages. Texas explicitly lets you report multiple employers for comp if your injury prevents you from working other jobs. Tips or irregular income are usually included if they were regular. Check your state’s rules or ask an attorney. - Q: Why am I not getting 100% of my old wage?

A: By law, workers’ comp is meant to replace only a portion of your lost income (to encourage return to work). The typical fraction is two-thirds. Plus, the benefit is limited by the state’s maximum weekly amount, even if your actual wage was higher. - Q: I still have questions – what should I do?

A: If you’re unsure about your calculation, don’t hesitate to get expert help. Many find that a quick conversation with a workers’ compensation attorney or claims adjuster can clarify ambiguities. Even a free consultation can tell you if you’re “working it out” correctly. For further reading, check your state labor department’s guidance or use an online workers’ comp calculator linked through state websites (many are available on state WCB or insurance sites).

Conclusion

Figuring out how to work out workers compensation doesn’t have to be a mystery. By methodically determining your Average Weekly Wage and applying your state’s formula, you can estimate the weekly benefits you should receive. We’ve covered the core steps – from computing AWW with gross pre-injury pay, to applying the legal percentage, and watching for state limits.

Remember the common pitfalls (like omitting overtime or miscounting weeks) so you don’t undercalculate your benefits. And keep in mind that if you settle, a simple estimate is to annualize your wage loss (weekly benefit × 52) and then adjust for future expenses. If in doubt, talk to a workers’ comp specialist or use a reputable calculator to double-check your numbers.

Want To understand Workers Compensation Rights – Read Our Detail Blog on Worker Compensation Rights