Every injured worker knows the pain of recovery , but did you know your state can greatly affect the Workers Compensation Benefits by State you receive? In the U.S., identical injuries can yield vastly different compensation depending on location. For example, In some states, you can get over $1,900 per week ,while others pay less than $600. losing an arm on the job in Alabama pays only about $48,840 (one of the lowest schedules in the nation), whereas that same injury in Illinois is worth $439,858. Alabama’s benefits are famously the country’s poorest, while a neighboring state like Georgia can be comparatively generous. This “geographic lottery” of benefits makes it crucial to understand each state’s rules, rates, and caps. In this guide we’ll explain what workers’ comp benefits cover, why they vary by state, and provide a side-by-side comparison of state maximum payouts. We’ll also highlight useful calculators, key factors that affect payouts, and answer common FAQs so you can navigate your claim confidently.

Workers compensation benefits provide income and medical coverage to employees hurt at work. In general, the benefits include:

- Wage replacement: Payments for time off work (temporary total, temporary partial, permanent total) – typically a percentage of pre-injury wages.

- Scheduled loss benefits: Set awards for loss of limbs, fingers, eyes, etc. (a “schedule” of values).

- Medical benefits: All necessary medical care, rehab, and even mileage for appointments.

- Death benefits: Support for dependents if a worker is fatally injured, including burial costs.

For example, Pond Lehocky attorneys note that “almost all states have a schedule of benefits” for specific losses, and include benefits for lost wages, lost body parts, medical care, and death. Together, these benefits are intended to cover the major costs of a work-related injury.

Types of Workers Compensation Benefits

Workers compensation benefits are divided into categories. Key types include:

- Temporary Total Disability (TTD): For when you can’t work at all for a period (generally pays about two-thirds of your average weekly wage in most states).

- Temporary Partial Disability (TPD): For when you can work in a limited capacity and lose some wages; usually a percentage of the wage difference.

- Permanent Partial Disability (PPD): A permanent impairment (e.g. loss of limb, partial loss of use) after healing – often tied to an impairment percentage or schedule.

- Permanent Total Disability (PTD): When a worker is permanently unable to return to any job. This often pays a high percentage of wages for life (or until a certain age).

- Specific Loss (Scheduled) Benefits: Lump sums or weekly amounts for losing a finger, arm, eye, etc., according to a state “schedule.” (For example, Alabama’s schedule pays only $48,840 for a lost arm, while Illinois pays $439,858.)

- Medical and Miscellaneous Benefits: Unlimited medical care, prescriptions, surgery, and even retraining costs. This also can include travel expense reimbursement to appointments.

Each state sets its own formulas. For example, in Colorado temporary benefits are generally two-thirds of the average weekly wage (capped at the state maximum). Massachusetts typically pays 60% of your pre-injury wage (subject to a min/max). The specific percentages and durations vary widely.

Why Benefits Differ by State

There is no federal standard for workers’ compensation benefits – it’s up to each state’s legislature and courts. “Each state has its own body of workers’ compensation law,” and every state (except Texas) requires employers to provide coverage, but the amounts and rules differ. Key reasons for differences include:

- Replacement Rate: Some states pay 66⅔% of your wages (e.g. Alabama, Georgia) while others use 70% (e.g. Mississippi), 75% (if high wages, some other jurisdictions), or even 100% of wages up to a cap (e.g. Florida’s cap is set at 100% of the state average wage). Texas is unique in not mandating coverage for most private employers, so many workers there may get no benefits at all.

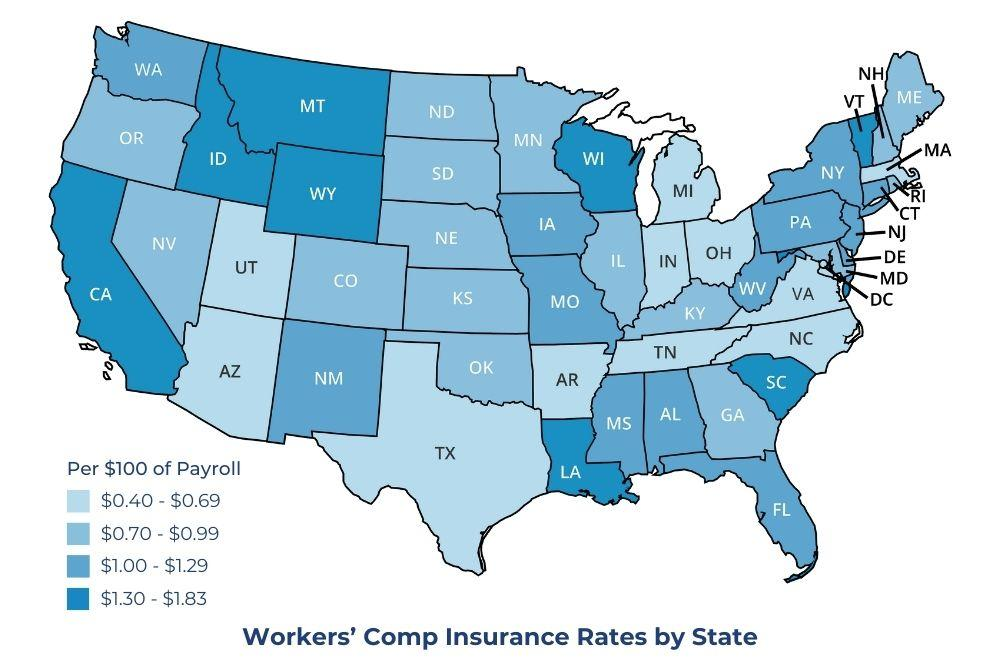

- Wage Caps: Each state caps the maximum weekly benefit by tying it to its own average wage. For example, Florida sets its cap at 100% of the state’s average weekly wage, while Colorado updates its cap each year (for 2025–26 it is $1,396.85). These caps can be double or more between states.

- Benefit Schedules: States list different values for lost body parts. Without any federal control, “it is totally up to states to determine their own benefits”. Alabama’s schedule has not changed in decades, whereas some states (like Illinois) have much higher amounts.

- Durations and Limits: Some states limit wage benefits to a set number of weeks (e.g. 500 weeks) while others pay until age 65 or longer. The trigger for permanent disability also varies (medical milestones vs. statutory timelines).

- Offset Rules: Some states reduce benefits if the worker is also eligible for Social Security Disability, while others (so-called “no-offset” states like Colorado) do not reduce the comp benefit.

- Medical Control & Misc Rules: States also differ on who directs medical care (employer vs. insurer), required forms, statutory waiting periods, and dispute processes.

In short, the combination of replacement percentage, wage cap, and rules can make one state’s benefits far more generous than another’s. As one commentator noted, “because Congress allows each state to set its own benefits, identical injuries can receive completely different benefits based on where they occurred”.

Workers Compensation Benefits by State (Comparison Table)

Below is a snapshot comparison of maximum weekly disability benefits in select states (2025–2026 figures). This illustrates the wide range: Massachusetts leads the nation’s caps at about $1,922 per week, while Georgia’s cap is only $575.

| State (Effective Date) | Maximum Weekly Benefit (approx.) | Notes / Replacement Rate |

|---|---|---|

| Massachusetts (Oct 1, 2025) | $1,922.48 | Uses 60% of wages (up to cap) |

| Colorado (Jul 1, 2025) | $1,396.85 | Pays 66⅔% of wages (capped) |

| Florida (Jan 1, 2026) | $1,358.00 | 100% of state average wage cap |

| Alabama (Jul 1, 2025) | $1,172.00 | 66⅔% of wages; very low schedule |

| Georgia (Jul 1, 2016) | $575.00 | 66⅔% of wages; nation’s lowest cap |

For context, many other states fall between these figures. The table highlights, for example, how Massachusetts’ cap is more than 3 times Georgia’s. States like Colorado and Florida are mid-range, tied to their higher cost-of-living wages. This table uses official state sources: Florida’s Dept. of Financial Services and Colorado’s Division of WC, along with state updates for Alabama and Georgia.

States with Highest Workers Compensation Benefits

- Massachusetts: Highest cap at about $1,922/week (effective Oct 2025). Pays roughly 60% of wages, subject to this high cap.

- Colorado: Max $1,396.85/week (Jul 2025), with 66⅔% wage replacement. Colorado also does not offset Social Security, making its true benefit even richer (it pays the full 66⅔%).

- Florida: Ties its cap to 100% of the state’s average wage – for 2026 that means $1,358/week. Although the replacement rate is effectively 66⅔% of your wages, the cap is high because Florida’s average wage is high.

- Alaska: Technically pays up to 120% of the state average weekly wage (subject to minimums). In practice, that has resulted in roughly $1,627/week in recent years (the highest single-state cap by a large margin). Alaska’s replacement rate is 80% of wages if your spendable earnings are below a threshold; otherwise 66⅔%.

- New York/New Jersey: (Not shown in table) These states also have relatively high benefits. For example, New York pays 66⅔% of post-tax wages up to a cap ($5,000/week in 2025) and New Jersey pays 70% of wages up to their cap (around $1,000+).

In general, states that tie their cap to a high average wage (MA, NY, NJ) or have high replacement percentages tend to give the highest benefits.

Workers Compensation Benefits by States with Lowest Benefits

- Georgia: Lowest cap at $575/week (effective 2016). Pays only 66⅔% of wages and has not raised its cap for years. Georgia is often cited as “the worst state” to be seriously injured.

- Alabama: While Alabama’s cap ($1,172) is not the absolute lowest, it has the lowest scheduled awards and among the lowest replacement rates. Notably, Alabama’s schedule for body parts is the poorest (e.g. an arm is only $48,840). The state recently started modest raises, but it still has the lowest awards for injuries.

- Mississippi: (Not in table) Pays 66⅔% up to a cap (about $1,000-ish in recent data). Historically among lower tier.

- South Carolina: Cap ~$1,134 (Jan 2026) – moderate, but SC has a very low replacement rate (55% for TTD) so actual benefits are smaller.

- Other Low States: Historically, states like Tennessee, Oklahoma, and Texas (which is optional) have been on the lower end in practice. Texas is unique: employers can choose to opt out of WC entirely (and buy private insurance), or not cover certain employees (like small businesses often skip it).

The contrast is dramatic: Georgia’s $575 max is literally the lowest, while some states have caps over $1,900. These extremes demonstrate why understanding your state’s rules is vital – an injury’s value can vary tenfold by location.

Useful Workers Compensation Calculators

When dealing with workers’ comp, various online tools can help estimate benefits. While actual payouts depend on state law and specifics, these calculators give ballpark figures:

- Workers Compensation Calculator: Estimates weekly wage benefits based on your salary and state rate.

- Injury Settlement Estimator: Roughly calculates lump-sum settlements for specific injuries.

- Lost Wage Calculator: Estimates time-off pay based on earnings and state wage-replacement rate.

- Disability Benefits Calculator: Computes payments for permanent disability (whole person impairment).

- Claim Timeline Estimator: Projects how long your claim process might take under typical state procedures.

- For More Tools: Visit www.toolsmaverick.cloud

(These tools vary by provider; many state bar or legal groups offer free calculators on their sites. For official rate info, check your state’s labor or insurance department website.)

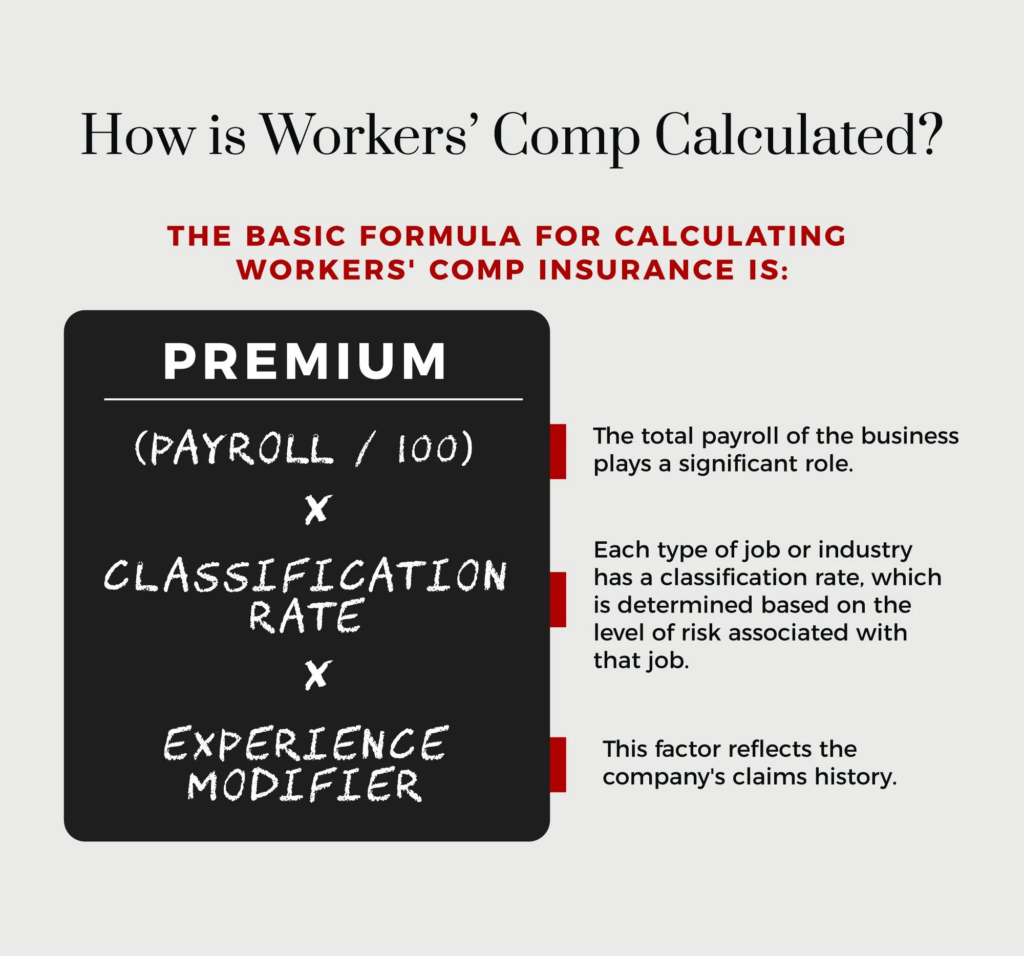

How Workers Compensation Benefits Are Calculated

At the heart of most WC calculations is your Average Weekly Wage (AWW). States typically use a formula (like averaging your last 26 or 52 weeks of gross pay) to determine pre-injury earnings. Then the state’s replacement rate is applied. For example:

- Many states (AL, GA, NJ, PA, etc.) use 66⅔% of AWW for total disability benefits.

- A few use 70% (MS, some outliers).

- Some like NY use 66⅔% of after-tax wages (so the actual check is close to 50% of gross).

- A few (e.g. Florida) are effectively 66⅔% up to a 100%-of-wage cap.

After applying the rate, the result is compared to the state’s minimum and maximum limits. If the calculated amount is above the max, it’s cut off. If below the minimum, it may be raised to the state’s floor. For example, Colorado’s law caps TTD at $1,396.85 (2025-26) and guarantees at least 2/3 of the state minimum wage. Alaska law actually ties the cap to 120% of the AWW.

Permanent injuries often use the same base rate but have additional scheduled formulas. For example, a 50% disability may pay 50% of the weekly TTD rate for a set number of weeks (varies by state and injury). Death benefits usually replace a portion (often 50%) of the wage for dependents. Each category (TTD, PPD, PTD, death) has its own computation, but all start from your AWW and the state’s rules. Understanding workers compensation benefits by state helps you estimate your payout.

How to Check Benefits in Your State

To get exact figures for your situation, check official state resources:

- State Labor/Industry websites: Most publish the annual AWW and max rates. For example, Florida’s Division of WC issues a bulletin each year (the 2026 rate is $1,358). Colorado’s DWC publishes the max benefit order (2025–26 cap $1,396.85).

- State statutes or codes: You can look up your state’s workers’ comp laws (many are online, as for Alaska). Or visit the state Department of Commerce/Labor site – e.g. the Mass.gov FAQ describes weekly benefits and caps for MA.

- Attorney or insurance guides: Law firms or insurance providers often summarize changes (like the Alabama “Compensation Rate Change” bulletin or the Georgia attorneys site). These are helpful for recent adjustments.

- National databases: The National Conference of State Legislatures or NCCI may have reports on average benefits by state. (Note: NCCI’s data is mainly for insurers, not the lay public.)

By checking these sources or contacting your state’s workers’ comp board, you’ll find the current max/min rates and formulas. Always use the rate corresponding to the injury date (some states base it on year of injury or date of loss).

Key Factors That Affect Your Benefits

Beyond state law, several personal factors influence your payout:

- Pre-injury wage: Higher earners hit the cap sooner (you’ll still only get the state max). Lower earners may get close to their full salary replacement, especially if the state allows above 66% for lower wages.

- Duration of disability: The longer you are disabled, the more you collect – up to any legal limit. Chronic injuries reaching permanent disability can extend benefits for years.

- Degree of impairment: Under permanent partial disability, the doctor’s impairment rating or limb schedule dictates the payout. A 10% impairment is 10% of the weekly rate for a certain number of weeks (varies by state law).

- Type of work: “Average weekly wage” calculations can differ for hourly vs. salary vs. commission jobs. States have rules about including overtime and bonuses.

- Offsetting Income: Some states reduce comp if you’re earning partial wages on light duty, or if you qualify for Social Security benefits (the “coordination” rules).

- Local cost of living: Indirectly, higher-wage states have higher caps, which means cost of living affects benefit levels.

In short, your actual benefit is determined by your wages × state rate, bounded by state caps and adjusted for any other income. Careful record-keeping of earnings and clear medical documentation will ensure you get the full amount owed under your state’s system.

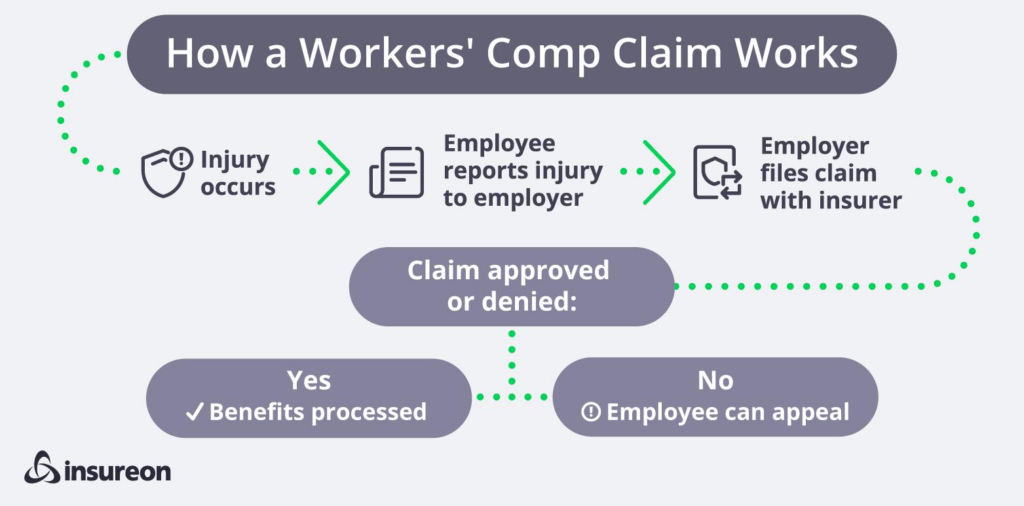

📝 How the Workers Compensation Claim Process Works

Filing a workers compensation claim is usually a simple step-by-step process. First, you must report your injury to your employer as soon as possible. Next, seek medical treatment from an approved doctor based on your state’s rules. After that, you’ll need to submit a claim form, which starts the official process. The insurance company will then review your claim, and if approved, you’ll begin receiving benefits such as medical coverage and wage replacement.

FAQs (Common Questions)

Q: Can I get benefits if I move to another state after my injury?

A: Typically, benefits are determined by the laws of the state where the injury occurred. If you move temporarily for work, some states adjust payments based on local wages, but generally your claim stays under the original state’s rules.

Q: How long do I get paid?

A: It depends on the injury. Temporary benefits last until you reach medical stability. Some states cap total payments (e.g. 500 weeks of permanent disability). Death benefits may be payable to surviving dependents for a set number of years or life.

Q: Why isn’t my benefit 100% of my salary?

A: Almost all states cap replacement at a fraction (commonly 66⅔%). The idea is partial wage replacement. Those caps protect employers/insurers from paying full salary forever. You keep a portion of your wages, and UI may cover some.

Q: How is Texas different?

A: Texas allows but does not require comp insurance. Many Texas businesses opt-out (called “the Texas model”) which leads to fewer covered injuries and no guaranteed benefits for many workers. If an employer does have comp, the rules (and caps) still differ from federal.

Q: Where do the calculators get their numbers?

A: They typically use your entered wage and state rates (often the official max limit) to estimate. They provide a rough figure, but actual claims depend on paperwork and approval by the state or insurers. Always verify via official tables.

For specific guidance, consider talking to a workers’ compensation attorney or your state’s compensation board. Many states also have consumer guides to their WC systems online.

Conclusion

Understanding workers compensation benefits by state is crucial for any injured worker. Each state’s laws create a different “picture” of what you may receive – from Georgia’s meager $575 cap to Massachusetts’s generous $1,922. While this guide highlights the major differences and highest/lowest examples, always check your specific state’s rules. Use tools (calculators, state websites) and professional help to estimate your benefits accurately.

Your experience matters: have you navigated a workers’ comp claim in different states? Share your thoughts or questions below to help fellow readers. If you found this comparison useful, consider subscribing for updates on labor law changes, or contact a qualified attorney to review your claim. Understanding your rights and the numbers at stake empowers you to advocate for the compensation you deserve.

Always check workers compensation benefits by state before filing a claim..

Pingback: Workers Compensation Claim Process (Easy Steps 2026)