Introduction

Getting hurt at work is already stressful enough. But then you find out your worker comp settlements offer is way lower than you expected, and suddenly you are dealing with financial pressure on top of physical pain.

Here is the truth most people never hear: the first offer from an insurance company is almost never the best offer. Worker comp settlements are negotiable, and the amount you walk away with depends heavily on what you know and how well you prepare.

This guide breaks down 7 proven ways to increase your payout, what mistakes to avoid, how insurance companies try to reduce what they owe you, and when it makes sense to hire a lawyer. Whether your injury is minor or serious, this information can make a real difference in your final settlement amount.

Why Most Worker Comp Settlements Are Lower Than Expected

Most injured workers accept their first offer without questioning it. That is exactly what insurance companies count on.

The average worker does not know how settlements are calculated. They do not know what they are legally entitled to, and they do not know that medical evidence, future costs, and lost earning capacity all play a role in determining what your case is actually worth.

Worker comp settlements are often low for a few key reasons. Insurance adjusters are trained to minimize payouts. Injured workers sometimes miss deadlines or fail to report all symptoms. Medical records are incomplete or missing. The injured person simply does not know their rights.

Understanding why settlements come in low is the first step toward doing something about it.

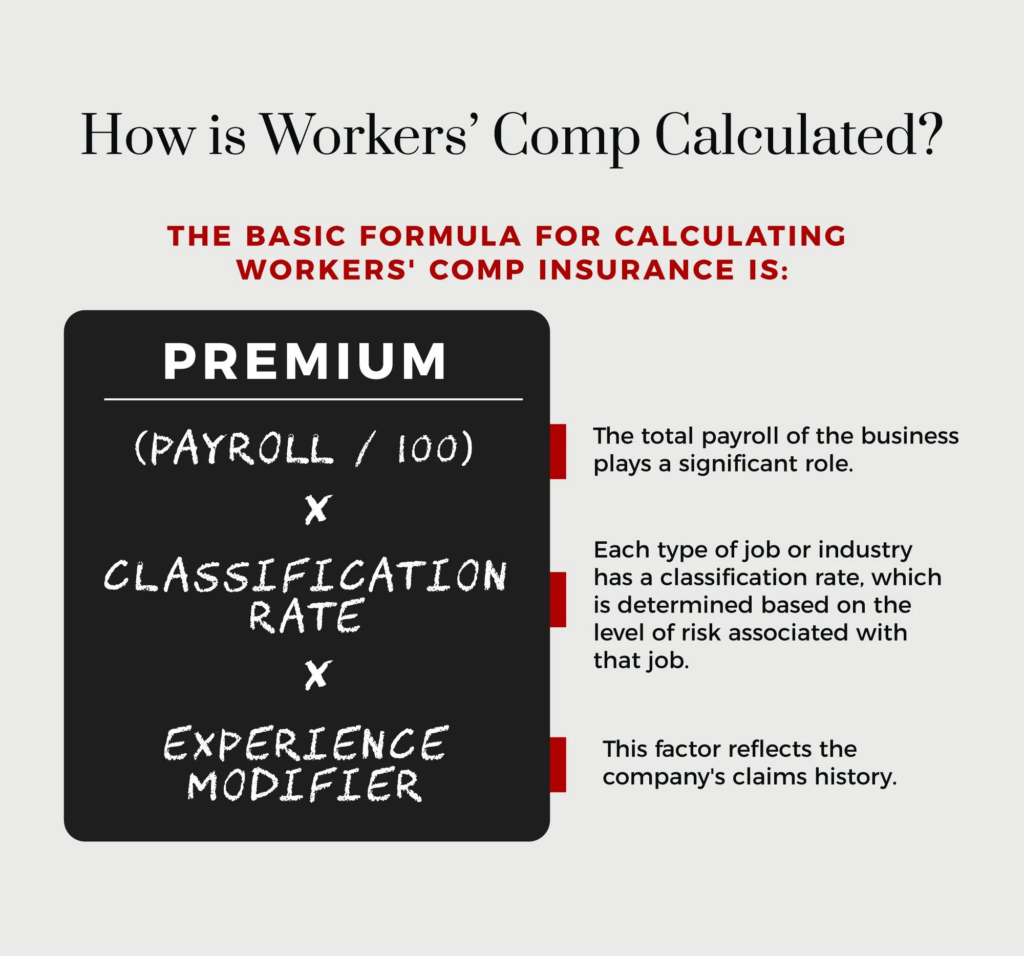

How Worker Comp Settlements Are Actually Calculated

Before you can increase your payout, you need to understand what goes into calculating it.

Worker comp settlements are based on a combination of factors including your average weekly wage, the severity of your injury, your permanent disability rating, future medical costs, and your ability to return to work.

Insurance companies use a formula that typically multiplies your disability rating by your weekly wage over a set number of weeks. Each state has its own rules on how this works, which is why workers compensation benefits vary significantly by state.

The higher your disability rating and the greater your lost earning capacity, the higher your potential settlement. But getting those numbers to reflect reality is where most people fall short.

You can get a quick estimate of your potential benefits using this Workers Compensation Calculator to better understand what your case might be worth before entering negotiations.

The Biggest Factors That Increase Your Settlement

Several key factors have the most impact on raising the value of your worker comp settlements.

Permanent Disability Rating The higher your permanent impairment rating, the more your settlement is worth. Make sure your doctor documents every limitation you have, not just the obvious ones.

Future Medical Costs If your injury requires surgery, long-term therapy, or ongoing medications, those future costs must be factored into your settlement. Many workers forget to account for this.

Lost Earning Capacity If your injury means you cannot return to the same job or earn the same income, that lost future income is a major part of your settlement value.

Type of Injury Serious injuries like back injuries, spinal damage, or injuries causing permanent restrictions naturally carry higher value. If you suffered a back injury, you can read more about how those cases are handled in this Workers Compensation Settlements for Back Injury guide.

Pre-existing Conditions If your work made a pre-existing condition worse, that can still be included in your claim. Do not assume pre-existing issues disqualify you.

Mistakes That Can Reduce Your Settlement Amount

Many workers unknowingly hurt their own case. Here are the most common mistakes that lower worker comp settlements.

Waiting too long to report the injury is one of the biggest ones. Every state has a reporting deadline, and missing it can eliminate your right to benefits entirely.

Skipping medical appointments or not following your treatment plan gives the insurance company reason to argue your injury is not as serious as claimed.

Posting on social media while on a claim is another common mistake. Photos or updates that suggest you are more active than your injury allows can and will be used against you.

Accepting the first settlement offer without reviewing it carefully is perhaps the costliest mistake. Once you sign, you typically cannot go back and ask for more.

Also make sure you understand how the workers compensation claim process works from start to finish, so you do not miss any important steps.

How Insurance Companies Try to Pay You Less

Insurance adjusters are not on your side. Their job is to close claims for as little money as possible. Here is how they do it.

They may dispute the severity of your injury or claim it was pre-existing. They may schedule an Independent Medical Examination with a doctor who tends to minimize injuries. They may delay the process hoping you will accept less out of financial desperation. They may use recorded statements to find inconsistencies in your account.

Being aware of these tactics helps you avoid falling into these traps. Never give a recorded statement without consulting a lawyer first, and always get a second medical opinion if you feel your injury is being downplayed.

How to Negotiate a Higher Workers Comp Settlement

Negotiation is where the real difference in worker comp settlements happens. Here is how to approach it.

Start by knowing your minimum number. What is the least you can accept to cover all your current and future medical costs, lost wages, and disability? Never go below that number.

Gather strong medical documentation before you negotiate. The more evidence you have showing the extent of your injury and its impact on your life, the stronger your position.

Do not rush. Insurance companies use time pressure to push people into accepting less. If you can afford to wait, you usually get a better offer.

Use a professional estimate to anchor your demand. Tools like the Injury Settlement Estimator can give you a realistic starting point for negotiations.

Counter every low offer in writing with a clear explanation of why it is insufficient based on your medical evidence and financial losses.

When to Accept or Reject a Settlement Offer

Knowing when to say yes or no is critical with worker comp settlements.

You should consider accepting if the offer covers all your future medical needs, compensates fairly for your lost wages and disability, and you have received a full medical evaluation confirming you have reached maximum medical improvement.

You should reject the offer if it does not account for future treatment, if your recovery is still ongoing, or if your disability rating has not yet been finalized.

Getting a second opinion from an attorney before accepting anything is strongly recommended. Once you sign a settlement agreement, it is almost always final.

How Medical Evidence Impacts Your Payout

Medical evidence is the foundation of any strong worker comp settlements case. Without it, you have very little to negotiate with.

Your medical records need to clearly document your diagnosis, how the injury happened at work, all symptoms including pain and limited range of motion, any permanent restrictions, and your prognosis for the future.

If your doctor is vague or dismissive, consider requesting a different treating physician or seeking a second opinion. A clear, detailed medical record makes it much harder for insurers to argue your injury is minor.

Should You Hire a Lawyer to Increase Settlement

This is one of the most common questions people ask about worker comp settlements, and the short answer is usually yes.

Studies consistently show that injured workers who hire attorneys receive significantly higher settlements than those who do not. A workers comp attorney typically works on contingency, meaning they only get paid if you win.

They know the true value of your case, can gather stronger medical evidence, handle all communication with the insurer, and will fight any unjust denials.

If you are unsure whether legal help is right for your situation, this guide on Do I Need a Lawyer for Workers Compensation breaks it down clearly.

Real Examples of Settlement Increases

Here are some realistic scenarios showing how following these strategies can make a difference.

| Scenario | Without Strategy | With Strategy |

|---|---|---|

| Back injury, no lawyer | $18,000 | $42,000 |

| Shoulder surgery, incomplete medical records | $25,000 | $55,000 |

| Permanent partial disability, first offer accepted | $30,000 | $70,000+ |

These are not guarantees, but they reflect the real difference that preparation, documentation, and negotiation make in worker comp settlements outcomes.

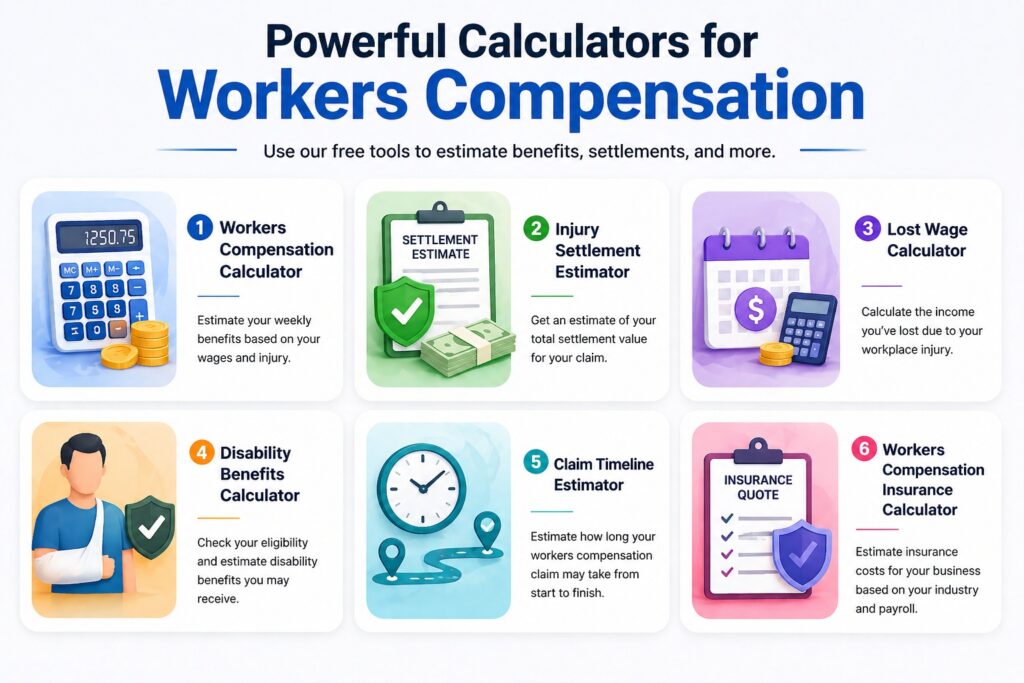

Tools to Estimate Your Settlement Value

Before you negotiate, you need a realistic idea of what your case is worth. These free tools can help.

The Workers Compensation Calculator helps you estimate your weekly benefits based on your wage and state rules.

The Injury Settlement Estimator gives you a rough range for your total settlement based on injury type and severity.

The Lost Wage Calculator helps you figure out how much income you have lost during recovery.

Use these together to build a clear picture of the compensation you deserve before walking into any negotiation.

Calculate your saving With Saving Calculator

Tips to Maximize Your Workers Compensation Money

Here is a quick summary of the most practical things you can do to increase your worker comp settlements payout.

Report your injury immediately and get it properly documented. See a doctor right away and follow all treatment recommendations. Keep a written journal of your symptoms, pain levels, and how your injury affects your daily life. Gather all evidence including witness statements, accident reports, and photos. Do not discuss your case on social media. Never accept the first offer without reviewing it carefully. Hire an attorney if your case involves serious or permanent injury. Get your disability rating reviewed if it seems low. Factor in future medical costs before agreeing to anything. Use online calculators to understand your case value before negotiations begin.

FAQs: Common Questions About Worker Comp Settlements

How long do worker comp settlements take? Most cases settle within 6 to 18 months, but complex cases with serious injuries or disputes can take longer.

Can I reopen my case after settling? In most cases, no. Once you sign a settlement agreement it is typically final. This is why reviewing every offer carefully before signing is so important.

What is a lump sum settlement? A lump sum settlement means you receive your entire compensation in one payment rather than over time. It often involves some negotiation on the total amount.

Do I have to pay taxes on my settlement? Workers comp settlements are generally not taxable, but there are some exceptions. Learn more in this detailed guide on Workers Compensation Benefits Taxable Income IRS Rules.

What if my claim was denied? A denial is not the end. You have the right to appeal. Getting legal help at this stage is strongly recommended.

Conclusion

Worker comp settlements are not set in stone. The amount you receive depends largely on how prepared you are, how strong your medical evidence is, and whether you understand your rights.

By avoiding common mistakes, gathering solid documentation, using the right tools to estimate your value, and seriously considering legal help for serious injuries, you can significantly increase what you walk away with.

Do not let an insurance company decide what your injury is worth. You have options, and now you have the knowledge to use them.

If you found this helpful, share it with someone who might be going through a workers comp claim right now. And feel free to use the free calculators linked throughout this post to get a realistic picture of your case before your next negotiation.