Introduction

If you are receiving disability benefits or about to apply, one of the biggest questions on your mind is probably this: are disability benefits taxable?

It is a fair question, and the answer is not always simple. Some disability payments are completely tax free. Others get taxed just like a regular paycheck. And a lot of people find this out the hard way, when they get a surprise tax bill at the end of the year.

This guide breaks everything down in plain, simple language. Whether you are getting Social Security Disability Insurance (SSDI), long term disability from your employer, or benefits from a private policy you paid for yourself, you will find your answer here.

Let us start from the beginning.

Are Disability Benefits Taxable? (Quick Answer)

The short answer is: it depends.

Are disability benefits taxable? Yes, sometimes. But not always. The tax rules are based on two main things: where the money is coming from and how much total income you have for the year.

Here is a quick summary:

Social Security Disability (SSDI) may be taxable if your income is above a certain limit. Long term disability from your employer is usually taxable. Benefits from a private policy you paid for yourself are generally not taxable. VA disability benefits and workers comp payments are not taxable.

We will go deeper into each of these below.

Which Disability Benefits Are NOT Taxable

There are several types of disability payments that the IRS does not tax at all. Here is what falls into the tax free category:

VA Disability Benefits: If you are a veteran receiving disability compensation from the Department of Veterans Affairs, that money is completely tax free. It does not matter how much you receive.

Workers Compensation: Money you receive from a workers comp claim after a job injury is not considered taxable income. If you want to understand more about this, check out this guide on Are Workers Compensation Benefits Taxable which covers the IRS rules in detail.

SSI (Supplemental Security Income): This is different from SSDI. SSI is a needs based program and is not taxable under any circumstances.

Private Disability Insurance You Paid For: If you bought a disability policy on your own using money you already paid taxes on, then the benefits you receive are not taxable.

Gifts and Welfare Payments: Any disability related financial assistance from nonprofit organizations or government welfare programs is also usually tax free.

When Disability Benefits Become Taxable Income

Now here is where it gets a little tricky.

Disability benefits become taxable when they come from a source that used pre tax dollars, or when your total income goes above the IRS limits.

The most common situations where people end up owing taxes on disability income include:

Employer paid disability insurance where your company paid the premiums. SSDI when your combined income is above the threshold. Group disability plans where premiums were paid with pre tax money.

Think of it this way: if you never paid taxes on the money that funded the benefit, you will likely pay taxes when you receive it.

Are Social Security Disability Benefits (SSDI) Taxable

This is the most common question people ask: are disability benefits taxable when they come from Social Security?

The answer is: maybe.

The IRS uses something called combined income to decide. Combined income is your adjusted gross income plus any non taxable interest plus half of your Social Security benefits.

Here is how it works:

If your combined income is below $25,000 (single) or $32,000 (married filing jointly), your SSDI is not taxable at all.

If it is between $25,000 and $34,000 (single), up to 50% of your benefits may be taxable.

If it is above $34,000 (single) or $44,000 (married), up to 85% of your benefits may be taxable.

So if you have other sources of income alongside your SSDI, like a part time job, pension, or investment income, you could end up owing taxes on a portion of your disability payments.

Are Long Term Disability Benefits Taxable

Are disability benefits taxable when they come from a long term disability plan? In most cases, yes.

If your employer pays for your long term disability insurance, the benefits are taxable income. This is because you never paid taxes on the premiums.

If you pay for your own long term disability insurance using after tax money, the benefits are not taxable.

Many people do not realize this until they are already receiving benefits. If your employer offers disability coverage as part of your benefits package, there is a good chance the payments will be taxed when you use them.

Employer Paid vs Self Paid Disability Insurance Taxes

This is one of the most important distinctions in disability tax law.

Who paid the premium decides who pays the tax.

| Situation | Are Benefits Taxable? |

|---|---|

| Employer pays 100% of premiums | Yes, fully taxable |

| You pay 100% with after tax dollars | Not taxable |

| Both employer and employee share premiums | Partially taxable |

| You pay with pre tax payroll deductions | Yes, taxable |

Many people assume that because they “have” disability insurance through work, they are protected. They are, but they may also owe taxes on every payment they receive. That is something worth knowing before you need the benefit.

Why Some People Pay Taxes on Disability Benefits

Are Disability Benefits Taxable ? It comes down to one core IRS principle: if income was never taxed before, it will be taxed when received.

When your employer pays disability premiums on your behalf, that money was never included in your taxable wages. So when you start receiving benefits, the IRS treats it as income you have never paid taxes on, and it taxes you then.

The same logic applies to SSDI when your overall income is high enough.

Also, some people receive back pay from Social Security, which is a lump sum for months or years of benefits that were delayed. This can push your income for one year very high, making more of it taxable. The IRS has a rule called the lump sum election method that may help in that case, but it requires some calculations.

How IRS Calculates Taxes on Disability Income

For SSDI, the IRS uses the combined income formula mentioned earlier. For employer sponsored long term disability, the full benefit amount is added to your gross income and taxed at your regular income tax rate.

There is no special flat tax rate for disability income. You pay based on your tax bracket.

For example, if you are single and your total income puts you in the 22% tax bracket, your taxable disability income is taxed at 22%.

This is why it is smart to either have taxes withheld from your payments upfront or make quarterly estimated tax payments to avoid a big bill in April.

What Happens If Taxes Are Not Withheld

If you do not have taxes withheld from your disability payments, and you owe money at the end of the year, you could face:

A large tax bill in April. Underpayment penalties from the IRS. Potential interest charges on the amount owed.

You can ask Social Security or your disability insurance provider to withhold federal taxes from your payments. For SSDI, you fill out Form W4V to request voluntary withholding.

Can You Avoid Taxes on Disability Benefits

In some cases, yes. Here are a few legal ways to reduce or avoid taxes on disability income:

Pay your own disability insurance premiums with after tax dollars so the benefits come back to you tax free.

Keep your total income below the IRS thresholds for SSDI taxation.

Use tax deductions and credits to lower your overall taxable income.

Consider filing separately if married, though this does not always help and can sometimes make things worse.

Work with a tax professional who understands disability income rules.

State Taxes vs Federal Taxes on Disability Payments

Federal tax rules are one thing. But are disability benefits taxable at the state level too?

It depends on your state.

Most states follow the federal rules and do not tax SSDI if the federal government does not. However, some states do tax disability income regardless of federal rules.

States that generally do not tax SSDI: Florida, Texas, Nevada, Washington, and others with no state income tax.

States that may tax disability income: California, Connecticut, Minnesota, and a few others have their own rules.

Always check your state’s tax laws or speak with a local tax advisor to understand what applies to you.

Disability Benefits and Tax Filing Requirements

Do you have to file a tax return if disability benefits are your only income?

If your only income is SSI, no. SSI is not taxable and does not count toward the filing threshold.

If your only income is SSDI and it is below the base amount ($25,000 for singles), you likely do not need to file.

If you have SSDI plus other income, you probably do need to file.

If you receive taxable long term disability benefits, you should file and report that income.

When in doubt, file anyway. It protects you and may even get you a refund if too much was withheld.

Common Tax Mistakes People Make

Here are the most common errors people make when dealing with disability income taxes:

Assuming all disability income is tax free. Many people think disability payments are never taxed. That is not true.

Not reporting SSDI on their return. Even if none of it ends up being taxable, you still need to include it when calculating combined income.

Forgetting back pay. A lump sum SSDI payment for prior years can mess up your income for the current year. There are IRS methods to handle this correctly.

Missing deductions. People on disability often qualify for extra deductions they do not claim.

Not estimating quarterly taxes. If your payments are taxable and nothing is withheld, you may owe a penalty.

Real Examples of Taxable vs Non Taxable Disability Income

Example 1: Maria is single, receives $15,000 in SSDI and has no other income. Her combined income is $7,500 (half of SSDI). This is below $25,000, so none of her SSDI is taxable.

Example 2: James is single, receives $18,000 in SSDI and earns $20,000 from a part time job. His combined income is $29,000. Up to 50% of his SSDI may now be taxable.

Example 3: Linda receives long term disability from her employer at $2,500 per month. Her employer paid 100% of the premiums. All $30,000 she receives that year is fully taxable income.

Example 4: Tom bought his own disability policy and pays the premiums himself with after tax money. He receives $2,000 per month during recovery. None of it is taxable.

How Disability Benefits Affect Other Income

Are disability benefits taxable in a way that changes your other deductions or credits? Yes, it can.

Receiving disability income can affect:

Your eligibility for the Earned Income Tax Credit (disability income is not earned income, so it does not count for EITC).

Your eligibility for premium tax credits if you are on a marketplace health plan.

Your ability to contribute to an IRA (you need earned income for that).

Social Security benefits calculations if you return to work.

It is also worth noting that if you are on workers comp and disability at the same time, there may be offset rules that reduce one payment based on the other. You can read more about how compensation and disability intersect in this guide on Workers Compensation Benefits by State.

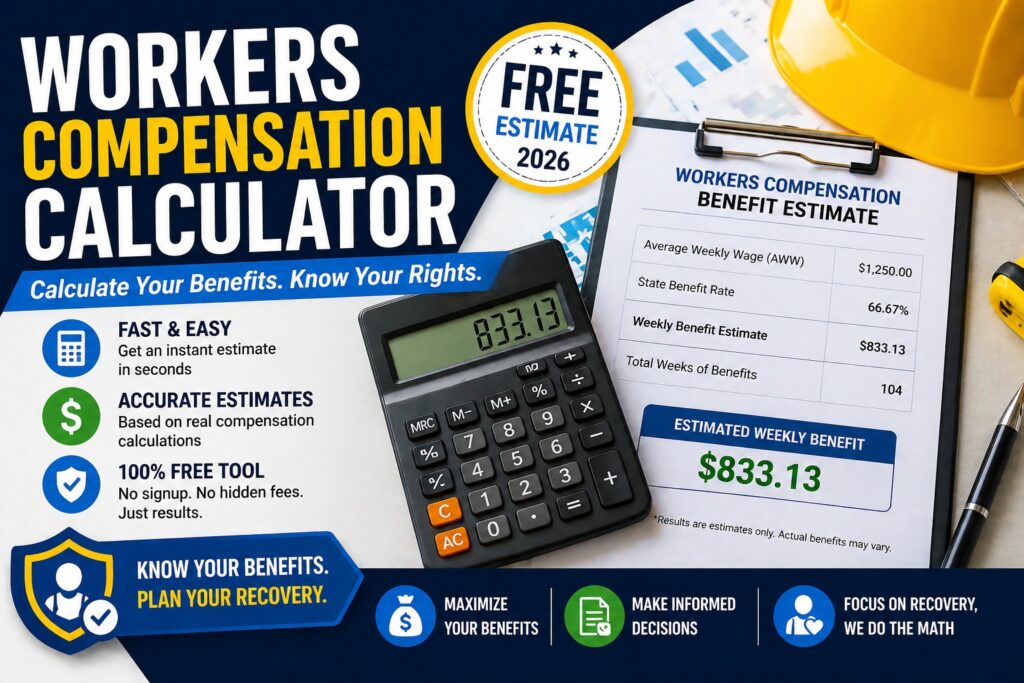

Tools to Estimate Benefits and Payments

Not sure how much you might receive or how taxes could affect your take home amount? These free tools can help:

Use the Disability Benefits Calculator to get an estimate of what you may be entitled to based on your situation.

If your disability is work related, the Lost Wage Calculator can help you figure out what income you may have missed during recovery.

These tools are free, easy to use, and give you a starting point before speaking with a professional.

Sponsored: 80+ Free Online Tools : www.toolsmaverick.cloud

FAQs

Is SSDI always taxable? No. It only becomes taxable if your combined income goes above $25,000 for singles or $32,000 for married couples.

Are disability benefits taxable if I am on SSI? No. SSI is never taxable.

Do I need to report disability benefits on my tax return? If you receive SSDI and have other income, yes. If your only income is SSI, no.

Are VA disability benefits taxable? No. VA disability compensation is completely tax free.

Can I have taxes withheld from my SSDI? Yes. You can file Form W4V to request voluntary federal tax withholding.

Are short term disability benefits taxable? It depends on who paid the premium. Same rules apply as long term disability.

Is disability income considered earned income? No. SSDI and most disability payments are not earned income, which affects certain credits and deductions.

Conclusion

So, are disability benefits taxable? The answer really comes down to what type of benefit you receive and your total income for the year.

SSI and VA benefits are never taxed. SSDI may be taxed depending on your other income. Employer paid long term disability is almost always taxed. Benefits from policies you paid for yourself are generally not taxed.

The most important thing you can do is understand where your benefits come from and plan ahead. Have taxes withheld if needed, keep track of all your income sources, and do not assume your disability payments are tax free without checking.

If you are dealing with a work injury or workers comp situation alongside disability, make sure you understand how the two interact. A great place to start is the Workers Compensation Claim Process guide which walks you through what to expect step by step.

And if you want to get a better estimate of what your benefits might look like, try the Disability Benefits Calculator before your next steps.

Disability income is already a difficult situation. Do not let an unexpected tax bill make it harder. Know your rights, plan smartly, and get the help you need.

Have questions about your specific situation? Drop them in the comments below or share this article with someone who might find it helpful.